You open up your banking app and see a strange deposit marked “ACH credit.” Are you being scammed? Can you keep the money? And do you need to do anything special to get it?

Take a deep breath. Though you might not recognize the name, an ACH credit is actually one of the most common forms of electronic funds transfer in America. In fact, yours is one of 29.1 billion payments made on the ACH network per year, according to Nacha.

Today, we’ll take a look at what ACH credits are, and how you can use them to send and receive money. We’ll also cover how your business can save money by using ACH, and how to get started today.

- What is an ACH credit?

- ACH Credit vs ACH Debit

- Are ACH credits safe?

- What do ACH credits cost?

- How long do ACH credits take to process?

- How to Use ACH Credits (as an Individual)

- How to Use ACH Credits (as a Business)

What is an ACH credit?

An ACH credit is a type of electronic payment. It uses a computer network called the Automated Clearing House to “push” money from the sender directly into the recipient’s bank account. It’s most commonly used for direct deposit paychecks, online tax refunds, or peer-to-peer payments.

ACH payments allow banks (or payment service providers) to transfer money from one account to another, without using checks, credit cards, or cash. This makes them extremely useful for repeat transactions, like payroll or recurring monthly payments.

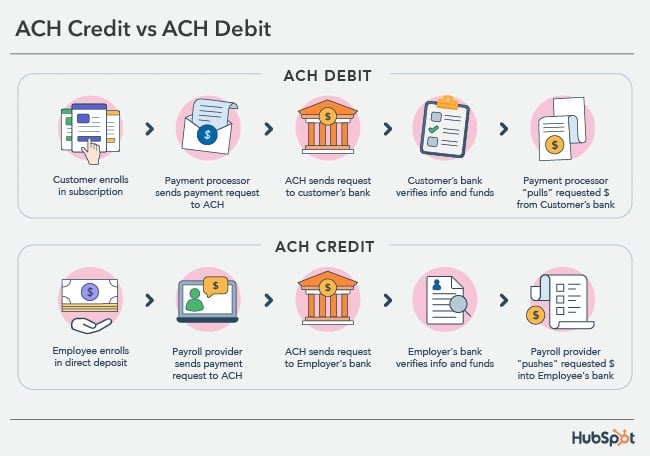

ACH Credit vs ACH Debit

ACH payments come in two flavors; credit or debit. The difference between the two lies in who initiates the transaction, and whether they’re “pushing” or “pulling” the money in your account.

- An ACH credit is initiated by the sender, and “pushes” money into the receiving account. An example of an ACH credit is a direct deposit paycheck.

- An ACH debit is initiated by the recipient, and “pulls” the money from the sending account. An example of an ACH debit is an auto-pay bill or a monthly subscription.

Keep in mind that not all online bill pay or subscriptions are handled via the ACH network. They may also use credit card, debit card, or wire transfer. Why does that matter? ACH payments are generally safer, cheaper, and more easily reversible.

If the transaction asks for your bank account or checking information, instead of your credit or debit card, it’s probably using the ACH network.

Are ACH credits safe?

It may seem unusual when a business asks for your banking details, but ACH payments are actually one of the safest forms of online payment. In fact, the Federal Reserve found that ACH credits have the lowest rate of fraud by value. That means it’s even safer than entering your credit card information.

Of course, you should always use caution when entering your personal information online. Stick to trusted websites that use up-to-date methods of security.

As a business owner, be sure to choose a payment processor that provides secure payment entry and keeps your customers’ data encrypted.

What do ACH credits cost?

There’s typically no cost to receive an ACH credit, but there may be fees involved if you’re the one sending it.

The cost of sending an ACH credit depends on the payment processor your business uses. These costs may include:

- A flat fee per transaction. These often run between $0.20 - $1.50.

- A percentage of the transaction. Typically 0.5 - 1.5%.

- A combination of the above.

For example, PayPal charges 3.49% plus $0.49 per transaction for ACH invoicing. On the other end, with HubSpot Payments you pay 0.5% of the transaction amount, capped at $10 max.

Be aware that some payment processors may also charge monthly service fees or initial setup charges. Make sure to compare total costs when considering a payment provider.

How long do ACH credits take to process?

If you’re on the receiving end of an ACH credit, it’s probably already in your bank account by the time you heard about it.

If you’re the one initiating an ACH credit, most experts recommend to budget for 3-5 business days for a standard ACH transaction. ACH rules require credits to be processed within 1-2 business days, but that depends on when the request was received. It also doesn’t include weekends or holidays.

Some ACH credits may be eligible for same-day or next-day processing, so you should ask your payment provider about those services.

How to Use ACH Credits (as an Individual)

Individuals aren’t typically able to send ACH credits. Usually, an individual making a payment through ACH is actually authorizing an ACH debit.

To receive an ACH credit, you’ll need to provide the sender with the same information you’d find on a paper check. This includes your:

- Name

- Routing number

- Bank account number

If you’re making a payment instead (an ACH debit), you’ll also provide an authorization for a certain dollar amount.

Either way, the business should provide you with a secure method to enter in these details.

How to Use ACH Credits (as a Business)

To get started sending ACH credits, you’ll need a merchant account or third-party payment processor. Many times this is already handled by your credit card processor, payroll services provider, or even your invoicing software.

If you’re just getting started with payment processing for the first time, there’ll be a short application process. For example, with HubSpot Payments, most accounts are ready to to begin making payments within 1-2 business days.

Once your account is approved, you’ll need a way to securely collect the recipients’ banking details. This is usually handled through a payment gateway that’s provided by your processor. A payment gateway is a piece of software that typically takes the form of a payment portal or checkout cart.

After you’ve got your payment processor and your payment gateway, you’re all set to start making ACH credits.

Credit Where Credit Is Due

As a recipient, you can rest easy that the ACH credit in your account is a trusted form of payment.

As a business, you can extend that same trust to your customers by offering ACH as an option. ACH payments are safe, simple, and can save you money.

![ACH API: What it is + How to Use it [+ Who Should Not]](https://blog.hubspot.com/hubfs/ach-api.jpg)